Market Commentary— The Big Get Bigger

Three quarters of the way through the year and it has certainly been an unusual one thus far. If one were to just look at headline numbers, it would probably be a pretty satisfying picture. After all, the Nasdaq and S&P 500 were up more than 27% and 13% through the first nine months. However, that hardly tells the whole story. The headline indices have been helped generously by a few of their larger components, dubbed the Magnificent Seven – Nvidia, Tesla, Meta (formerly known as Facebook), Microsoft, Apple, Alphabet (formerly known as Google), and Amazon. For those that do not own those securities, it’s been a much different sort of year.

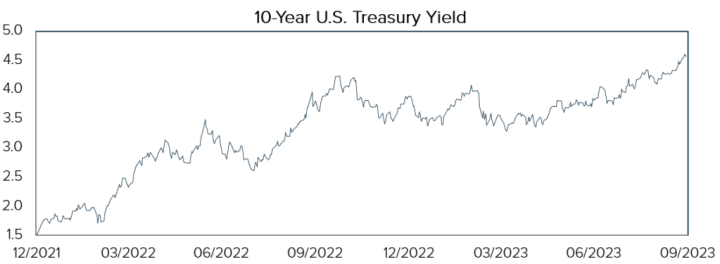

While the stock market has risen, pain has resumed in the bond market as interest rates have begun to rise once more. The Bloomberg US Aggregate Index, which can serve as a broad gauge for the bond market, is on pace for its third consecutive down year – its first such negative streak since the mid-2000s. Treasuries with longer maturities are also on pace for the third consecutive down year – a first since the early ‘80s.

Last year, interest rates were rising largely due to inflationary pressures, which acted as a headwind for the equity market. Generally speaking, as interest rates rise, it would be reasonable to expect that stock valuations would decline. This is one of the reasons why stocks had a tough year in 2022 – inflation was leading to higher interest rates, which had the expected effect on stock prices. A little bit of stability in the bond market between October of 2022 and August of this year allowed equities to find their footing. However, since early August, interest rates have started moving higher once more. This time around, it likely has less to do with inflation. However, the end result is largely the same. As yields have risen, volatility in the stock market has risen too – acting as a headwind for the market.

Despite this, the S&P 500 was still up double digits through its first nine months! However, a shortcoming of the S&P 500, or the tech-laden Nasdaq, when being used as a measuring stick is that they are overly influenced by the biggest companies. This year, both indices have been carried by their largest components, an AI boom, and the aforementioned “Magnificent Seven”. Last year, for the most part, those stocks were anything but! Those same names that have soared this year were largely singing a much different tune throughout 2022. Nvidia, for example, at one point had fallen 60+% in 2022, while Meta fell more than 70% from its peak to its trough. Both have rebounded and have surged more than 200% this year, which has skewed the index and propelled it higher. Yet the average stock has not participated nearly to the same extent. In that same vein, the average stock did not participate nearly as much to the downside in 2022.

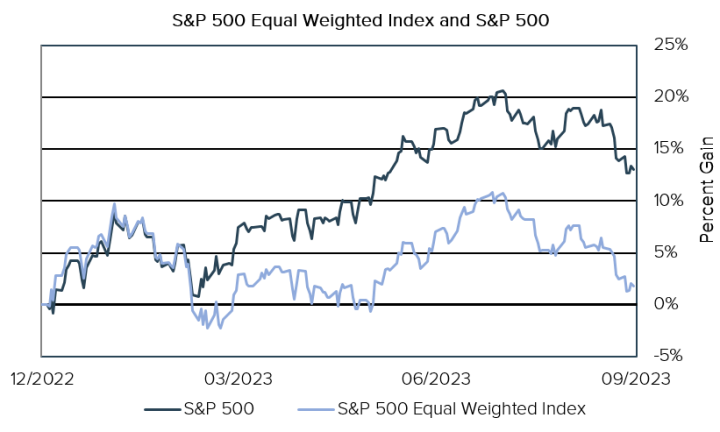

If one is trying to get a gauge of the average stock, rather than just the largest stocks, then perhaps those indices aren’t the best measuring sticks. The S&P 500 Equal Weighted Index, on the other hand, can be viewed as a measure of the “average” stock in the S&P 500. While the traditional S&P 500 weighs stocks by market capitalization (or size), the equal-weighted version of the index treats all companies equally. That index was up less than 2% through the first nine months of the year.

For the first two and a half months of 2023, the S&P 500 and its equal weighted counterpart traded more or less in lockstep. However, around the time that Silicon Valley Bank failed, soon to be followed by a few more banks, that relationship began to breakdown. Since then, the S&P 500 largely moved higher, while its equal weighted peer could best be described as treading water. The divergence between the average stock and the Magnificent Seven has widened precipitously as the year has passed. Not owning the Magnificent Seven was rewarding for most investors in 2022. This year, not owning those stocks has been a surefire way to underperform.

Recently, I was talking with a financial advisor partner of ours that asked about performance for the first nine months. While Tandem owns Microsoft in two of our three strategies, we do not own any of the other “Magnificent Seven” names. We aim, for better or worse, to provide a more consistent, more repeatable, and less volatile investment experience for those that entrust us with their assets. To do this, we seek out companies that display the consistent fundamental growth that we value throughout an economic cycle. The consistency of a company’s growth is paramount to our investment strategy. If a company does not meet our criteria for consistent growth, then it cannot be invested in. It’s that simple. A company either meets our criteria, and can therefore be added to the portfolio at the appropriate price, or it does not have the consistent growth we value and it will not enter the portfolio at all.

Now, it’s worth noting that we do not think a stock is a “bad” stock if it doesn’t meet our criteria. But if a stock doesn’t meet our criteria, it simply has no place in our portfolio. That doesn’t mean that folks shouldn’t own that stock in their overall investment portfolio. On that, we have no opinion! That conversation is best had between investor and financial advisor. Instead, for Tandem, it just means that we stick to our discipline. As a result, Tandem’s strategies are likely to have a different makeup than that of the broader market. We think that is a good thing.

Commentary— Two Pillars

The University of Virginia men’s basketball coach Tony Bennett has built a successful program in Tandem’s original hometown of Charlottesville, Virginia. Part of the key to success for the team has been Bennett’s “five pillars”: humility, passion, unity, servanthood, and thankfulness. Those pillars guide the team through good times, like winning a national championship, and through bad times, like when UVA became the first #1 seed to ever lose to a #16 seed during March Madness. Tandem has two such pillars when it comes to managing your money – though admittedly, they are a little wordier than Bennett’s five.

Our first pillar is that Tandem strives to deliver a more consistent, repeatable, and less volatile investment experience. It is our belief that volatility is the enemy of most investors. A select few may keep an even keel through good times and the bad, but most of us succumb to human nature and the temptation to make emotional decisions during stressful periods. We believe that volatility in the stock market creates a more hectic and stressful environment that can cause investors to act emotionally. Personally, very few of my emotional decisions have been among my best.

The tendency for most investors, individuals and professionals alike, is to become a bit euphoric when things go our way, and to become somewhat frantic when the tide turns against us. The degrees of euphoric and frantic sentiment generally correlate with the size of the market’s advance or decline. Bull markets are fun. We grow confident in them. We want more. We might even get a little FOMO (Fear Of Missing Out), which can cause some to chase markets higher. As a result of that over-confidence, or FOMO, some folks end up buying high – paying more than they should for something because they are convinced it will continue to go up and they don’t want to miss the ride. On the other hand, bear markets are not fun. We grow concerned. At some point in the decline, we just want out. The pain of seeing assets drop in value can be too much. And, as a result, some will panic and sell low – selling at lower prices because they have become convinced that markets will continue to go down indefinitely, and the stress has just become too much to bear.

In essence, it’s volatility that can get the best of most investors. Volatile markets to the upside can cause people to pay high prices because they fear missing out. Volatile markets to the downside can cause people to panic and sell low because they don’t want to see prices drop any further.

In 2009, Jack Bogle, the founder of one of the largest passive investing companies, Vanguard, published an interesting study on the average investor’s performance. In it, Bogle compared the returns of individual investors versus the funds that the investors owned. The funds outperformed by 4.5% annually due to poor timing from the individual investors. This is a significant difference between expected and actual return. In other words, investors chased performance higher when the market was up, and they often sold following periods of poor performance within those funds. Long story short, Jack Bogle (who is the father of passive investing!) found that the average investor will buy high and sell low – the exact opposite of what one should do, which is buy low and sell high.

Need more proof of the poor timing of one’s emotional decision making? According to the Investment Company Institute (ICI), stocks experienced massive inflows in 2000, which coincided with a major top in the stock market. Investors poured money into the market as it was setting its then all-time high. They bought high. Equities had outflows in 2002, 2008 and 2009 – all of which marked major market bottoms. They sold low. ICI proved that many investors routinely, in spite of themselves, bought high and sold low!

That brings us to our second pillar at Tandem. We truly attempt to practice the discipline of buying low and selling high. Shocker. It is Investing 101 after all. To make a profit, one needs to buy low and then sell high. If only it were so simple! What’s shocking though is that it may not always be commonplace, as evidenced by Bogle’s study. While it may not be commonplace, it certainly is commonsense. In our opinion, the best time to buy and the best time to sell do not always overlap. If they do not overlap, then one must have the discipline and patience to wait in between those two time periods.

Tandem will not buy something just because we sold something. Nor will we ever sell something just because we bought something. The decision to sell one stock is completely independent from the decision to buy another. If there are more stocks to sell than there are to buy, then cash will rise in a portfolio. If there are more stocks to buy than there are to sell, then cash levels will fall in a portfolio. That is how cash is managed within the Tandem portfolio. Never is there an overarching decision that cash and cash equivalents ought to be X% because of A, B, and C. Cash ends up where it ends up as a result of the individual decisions made within the portfolio.

Unfortunately, there is no such thing as a crystal ball for investing. There is no market timing panacea. In fact, it is our opinion that trying to time something is foolhardy. Instead, you must act when you believe probabilities are tilted in your favor. Probabilities do not equate to certainty. Just because something is probable, does not mean it will happen. It just means that it is more probable than not. So, when our model deems something to be “unsustainably overvalued” it does not mean the stock will begin trading lower immediately as it reverts back to its mean. It’s our belief that over time, the stock is more likely to mean-revert, so the prudent action is to take some money off the table. That is how we try to sell high. Now, our model is not a crystal ball. It is not perfect. As such, we can occasionally be early. That’s okay. We prefer to leave a party too early, rather than leave a party too late once there is a dash for the exit.

Naturally, if one is comfortable with the notion of leaving a party early, then one must be comfortable with the idea of missing out on some of the fun. Investing is no different. If your goal is to buy low, then the cash must come from somewhere. In our process, that cash to buy low must come from having proactively sold high. In short, to successfully buy stocks at attractive entry prices, one must have capital available to do so. Within our portfolios, we believe the best way to have that capital available is to have previously sold stocks at attractive exit prices.

Ultimately, in our effort to limit volatility in a client’s portfolio, we attempt to invest in more consistent and less volatile businesses while also practicing the discipline of buying low and selling high. To us, this is commonsense. But it is not for everyone. To do this, there are certain stocks that we may just not own. For example, in Market Commentary, we discussed the recent performance of “The Magnificent Seven” year-to-date. Most of those stocks simply do not meet our stringent criteria. This does not mean they are bad companies, but it does mean that we believe they will likely produce an experience contrary to the one we seek. This means that for most of those names, they impact our portfolio very minimally. If those stocks we do not own do well, so be it, we will not participate in that. If those stocks we do not own perform poorly, all the better for us as we will not be participating in that either.

Recently a financial advisor partner asked us to explain our performance this year and what we might change moving forward. The answer is simple – nothing. We will not change our pillars. We attempt to do this one very specific thing – deliver a more consistent, repeatable, and less volatile investment experience. Sometimes that may cause some head scratching to watch as we leave a party early while attempting to sell high. It may be unnerving as we deploy capital in down markets in an attempt to buy low. It can be rewarding to not own stocks that are leading the market lower, just like it can be frustrating to not own ones, like most of the Magnificent Seven, that are leading the market higher.

Tony Bennett did not change his five pillars following UVA’s first round exit, which was one of the largest upsets in college basketball history. Some folks in Charlottesville probably would have loved to see some change. Instead, Tony Bennett stayed the course. Ultimately, he reached the pinnacle of his profession, winning a national championship just twelve months later.

At Tandem, regardless of whether our portfolio is up or down, whether it is beating its benchmark or trailing, we make this promise: we will continue to practice our discipline. We will continue to adhere to our pillars as we will always strive to deliver a more consistent, more repeatable, and less volatile experience while practicing the art of buying low and selling high. Those two things are woven into our very being as a company. All of this, we hope, is able to keep our clients invested. After all, if investors had just stayed the course in Jack Bogle’s study, then they would have experienced performance more similar to that of the funds that they were invested in. We believe staying invested is key – which doesn’t necessarily always mean all in, or all out. We aim to keep investors invested while hopefully providing a more palatable investment experience.

Tandem News

Tandem has grown its headcount once more. Our most recent addition joined us at the end of June. Nicki Hoffman joined the Tandem team as its new Chief Compliance Officer. Ms. Hoffman spent the previous 21 years at an Investment Advisory and Broker Dealer firm. In the past, Ms. Hoffman has done a little bit of everything, having worked as a Sales Assistant, Trader, Limited Partnership Coordinator, Executive Assistant, and for the past 15 years, Senior Compliance Officer. When Nicki is not in the office she enjoys exercising, traveling, and spending time with her husband and two boys. Please join us in welcoming Nicki to the team!

Share:

Disclaimer: Tandem Investment Advisors, Inc. is an SEC registered investment advisor.

This audio/writing is for informational purposes only and shall not constitute or be considered financial, tax or investment advice, or an offer to sell, or a solicitation of an offer to buy any product, service, or security. Tandem Investment Advisors, Inc. does not represent that the securities, products, or services discussed in this writing are suitable for any particular investor. Indices are unmanaged and not available for direct investment. Please consult your financial advisor before making any investment decisions. Past performance is no guarantee of future results. All past portfolio purchases and sales are available upon request.

All performance figures, data points, charts and graphs contained in this report are derived from publicly available sources believed to be reliable. Tandem makes no representation as to the accuracy of these numbers, nor should they be construed as any representation of past or future performance.

Insightful Updates

Delivered

Timely and engaging information—right to your inbox.

More Commentary

Notes from the Trading Desk

A post-election surge in U.S. stocks drove major equity indices to all-time highs last week. The S&P 500 surpassed 6,000 and logged its 50th record high of the year, while the Dow Jones Industrials Average crossed 44,000 for the first time.

Observations

Major U.S. equity markets experienced some consolidation in October after several months of upward momentum. The S&P 500 broke a streak of five consecutive monthly gains, declining 0.99%.

The Tandem Report

The stock market continued its impressive run in the third quarter—albeit with a small hiccup in early August. The S&P 500 closed 5.5% higher, which brought the year-to-date gain through September to nearly 21%.