Market Movers & Shakers

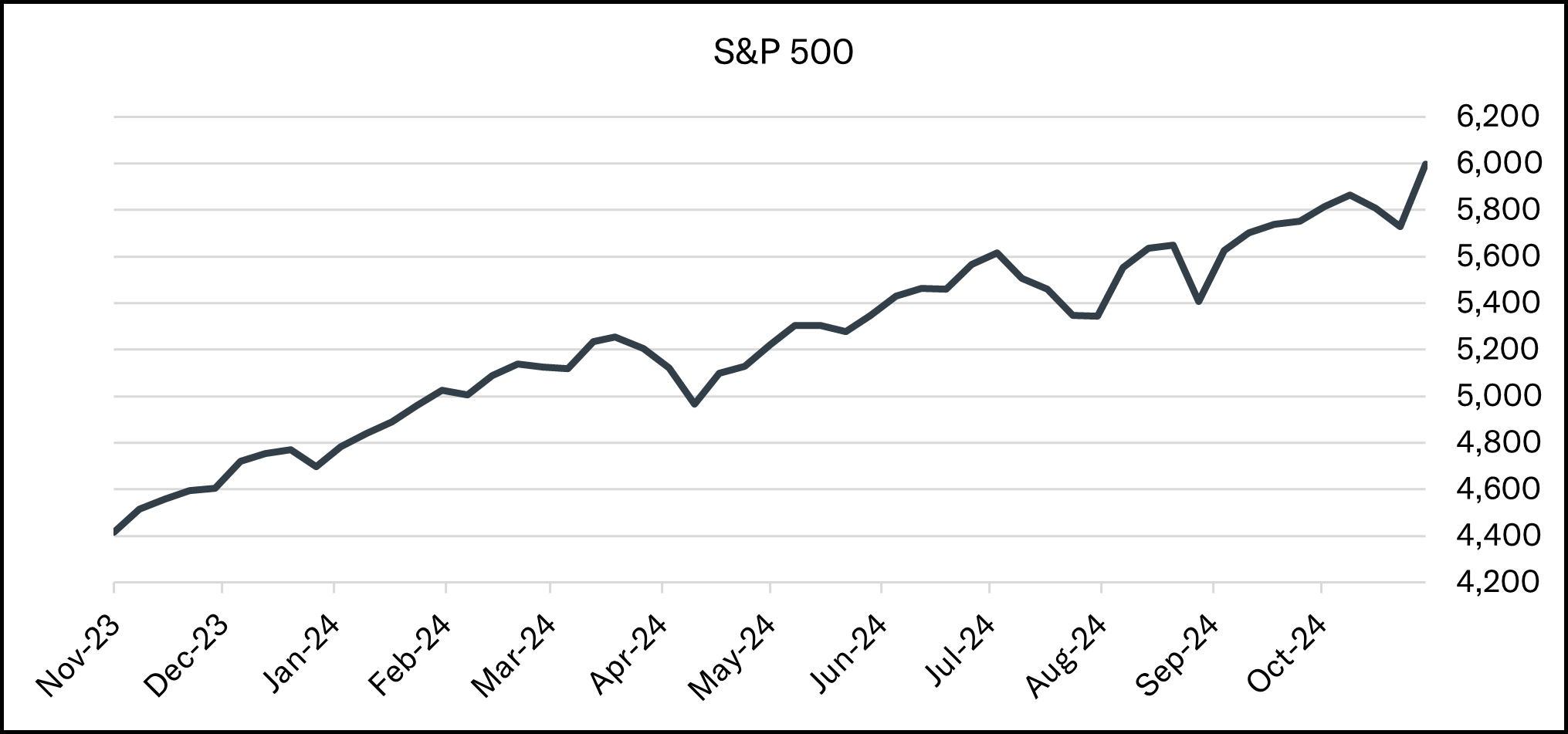

A post-election surge in U.S. stocks drove major equity indices to all-time highs last week. The S&P 500 surpassed 6,000 and logged its 50th record high of the year, while the Dow Jones Industrials Average crossed 44,000 for the first time. The S&P 500 and Dow finished up 4.66% and 4.61%, respectively, for the week, both posting their best weekly gains since November 2023. The tech-heavy Nasdaq outpaced those moves with a 5.74% advance while the small cap Russell 2000 index surged 8.57% for its best weekly performance since 2020. A quick and decisive election outcome and the prospect of reduced regulation and tax cuts under the new administration sparked a big rally across risk assets. All 11 sectors of the S&P 500 finished the week higher, with notable outperformance in Energy, Industrials, and Financials. Bank stocks in particular saw robust gains. The SPDR S&P 500 Regional Banking ETF (KRE) posted a 10.81% weekly gain, while some of the nation’s largest banks like Morgan Stanley and Goldman Sachs also logged double-digit gains. Treasury yields, particularly on the long end of the curve, initially spiked following the election results, driven by a mix of concerns that new tax and budget proposals could present upside risks to inflation and optimism for a more robust future growth outlook. The 10-year U.S. Treasury yield rose to as high as 4.48% on Wednesday before retrenching to pre-election levels by the end of the week, settling at 4.30%.

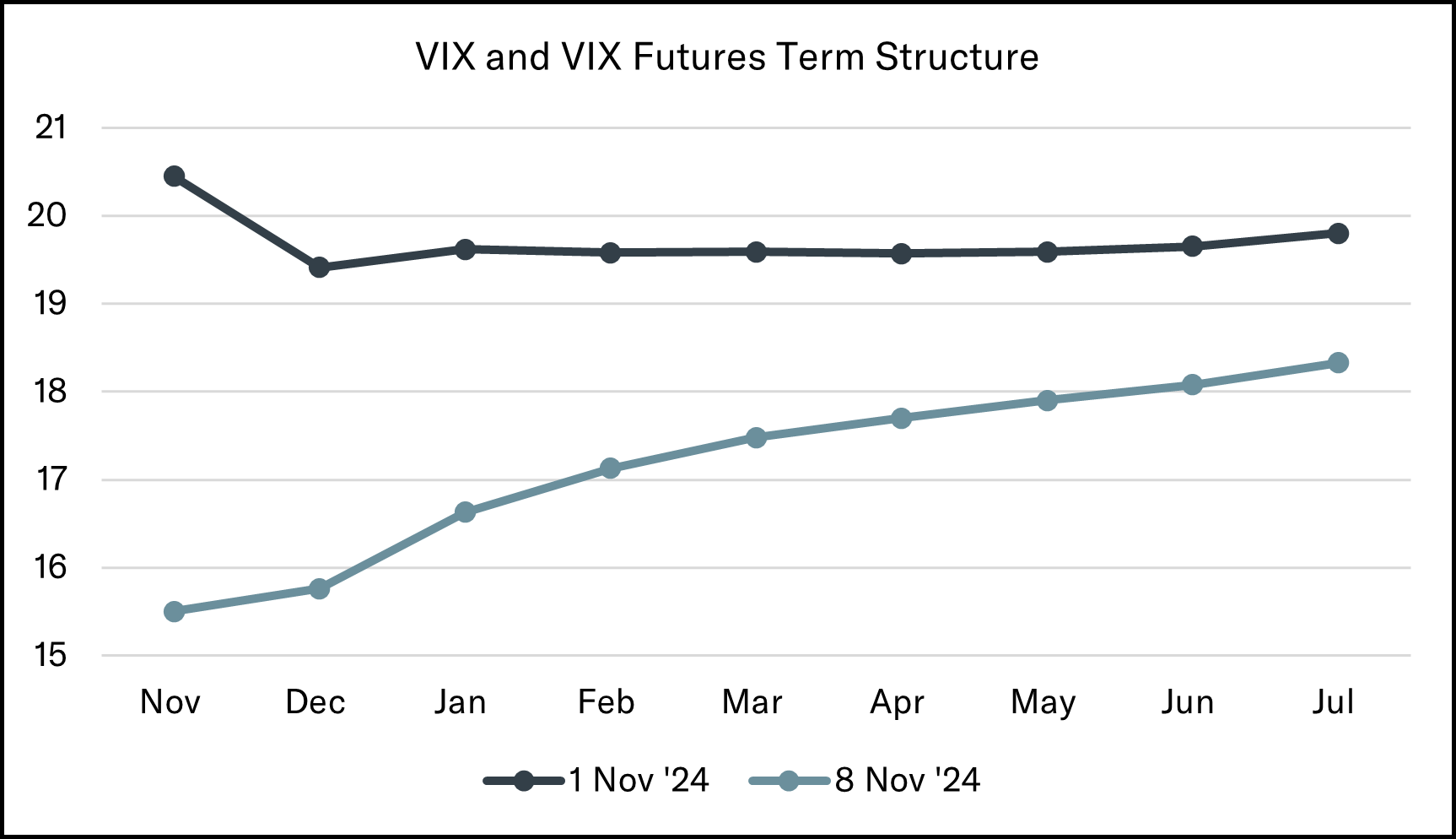

Volatility, as measured by the ICE BofA MOVE index on the fixed-income side and the CBOE Volatility Index (VIX) on the equity side, has retreated significantly now that the U.S. election is in the rearview. The VIX curve, also known as the VIX term structure, displays changes in implied volatility across different time horizons. The shape of the curve is normally upward sloping (contango) as the future becomes increasingly more uncertain the further out in time you go. However, during periods of heightened uncertainty, like during the COVID-19 market crash in early 2020, or ahead of a highly consequential event like a presidential election, short-term implied volatility can become elevated, causing the curve to invert (backwardation). And that is exactly what happened last month leading up to the election! In our last edition of Notes from the Trading Desk, we highlighted an elevated VIX despite markets being at or near all-time highs. The overhang of the election and uncertainty surrounding the length of time it would take to know a decisive outcome pinned November’s VIX futures contract higher than contracts expiring in subsequent months. A speedy and decisive outcome in the early hours of Wednesday, November 6th served to flush volatility out of the market, normalizing the term structure of volatility and retrenching the VIX below 15.

The Federal Reserve cut interest rates by 25 basis points last week at the November FOMC meeting, bringing the target range for the federal funds rate down to 4.5-4.75%. The widely anticipated rate cut was unanimous and followed a larger 50 basis point cut at the Fed’s September meeting. Takeaways from the meeting were that it was largely uneventful, with no significant changes to policy statement language or the forward outlook. Fed Chair Powell reiterated that the Federal Reserve will continue assessing incoming data to determine the “pace and destination” of interest rates as the Fed balances its dual mandate of maximum employment and price stability. Markets are currently pricing in a 65% chance of an additional 25 basis point rate cut at the FOMC’s December meeting, down from 83% one week ago.

Earnings season is now mostly in the books. According to FactSet, 91% of S&P 500 companies have reported their Q3 results. 75% of S&P 500 companies reported a positive EPS surprise while 60% of companies reported a positive revenue surprise. With 91% of companies reporting, the blended year-over-year earnings growth rate for the S&P 500 for Q3 2024 is 5.3%, which would mark the 5th straight quarter of year-over-year earnings growth for the index. Earnings estimates for Q3 had been revised lower throughout the summer from over 8% in June to just above 4% by the end of September. So, technically Q3 2024 EPS growth is on track to exceed estimates even though the bar had been significantly lowered. Looking ahead to the fourth quarter, at this point in time, 77 companies in the S&P 500 have issued EPS guidance for Q4. Of the 77 companies, 53 have issued negative EPS guidance and 24 have issued positive EPS guidance. The percentage of companies issuing negative EPS guidance for Q4 2024 is 69%, which is above the 5-year average of 58% and above the 10-year average of 62%. From a valuation standpoint, the forward 12-month P/E ratio for the S&P 500 is now 22.2, well above historical averages.

Updates & News*

A number of companies in Tandem’s portfolio reported quarterly results and were in the news since our last update here. Abbott Laboratories (ABT) was cleared of liability by a U.S. court in a case concerning their baby formulas. The lawsuit, which sought $6.2 billion in damages and was an overhang on the stock, claimed Abbott had failed to issue proper warnings about risks linked to using its specialized baby formulas. In a statement, Abbott said “the decision reinforces what we, the medical community and regulatory bodies have said: that preterm infant nutrition products are safe”. On the earnings front, Becton Dickinson (BDX) reported an EPS and revenue beat and provided upbeat guidance for fiscal 2025. The medical technology company recently acquired Edward Lifesciences’ critical-care unit, which makes heart monitors and other medical equipment, for $4.2 billion in cash, which has helped buoy sales. In addition to reporting a strong quarter, Becton Dickinson announced a 9.5% increase to its quarterly dividend, marking its 53rd consecutive fiscal year of dividend increases. And speaking of dividend increases, Automatic Data Processing (ADP) announced a 10% dividend increase last week, extending the company’s streak of payout increases to 50 years, while Roper Technologies (ROP) also announced a 10% increase to its quarterly dividend, marking 32 consecutive years of dividend growth. A recent addition to Tandem strategies, Genpact (G), reported third-quarter results that beat on both the top and bottom line and raised its forward guidance. Genpact noted in its earnings call that partnerships with hyperscalers like AWS, Microsoft, and Google are enhancing proprietary solutions and revenue growth. Elsewhere, Bloomberg reported that Qualys (QLYS) is exploring options including a potential sale after receiving takeover interest.

Source: Source of all data is FactSet, unless otherwise noted.

*The transition level activity taken by Tandem is applicable to new accounts and new money, not the composite or firm-wide level. New accounts and new money are not automatically invested on the first day. Rather, they are transitioned into our strategy over a longer time period that is dependent upon market conditions. Strategy level activity is applicable to the composite and action is taken at the firm-wide level.

Share:

Disclaimer: Tandem Investment Advisors, Inc. is an SEC registered investment advisor.

This audio/writing is for informational purposes only and shall not constitute or be considered financial, tax or investment advice, or an offer to sell, or a solicitation of an offer to buy any product, service, or security. Tandem Investment Advisors, Inc. does not represent that the securities, products, or services discussed in this writing are suitable for any particular investor. Indices are unmanaged and not available for direct investment. Please consult your financial advisor before making any investment decisions. Past performance is no guarantee of future results. All past portfolio purchases and sales are available upon request.

All performance figures, data points, charts and graphs contained in this report are derived from publicly available sources believed to be reliable. Tandem makes no representation as to the accuracy of these numbers, nor should they be construed as any representation of past or future performance.

Insightful Updates

Delivered

Timely and engaging information—right to your inbox.

More Commentary

The Tandem Report

With 2024 now in the books, it was certainly another good year for the S&P 500. The index gained more than 20% for the second consecutive year and the third time in the past four years.

Notes from the Trading Desk

U.S. stocks have stumbled out of the gate to start 2025, with the S&P 500 and Nasdaq both registering back-to-back weekly losses in the first two weeks of the year. The S&P 500 declined 1.94% last week, its fourth weekly decline in...

Observations

December painted a mixed picture across U.S. financial markets with varied performance among major indices. The S&P 500 declined by 2.50%, while the small-cap Russell 2000 suffered a sharp 8.40% loss and nearly gave back all of November’s huge gains.