Market Commentary— AI-Related Companies Driving the Market Higher

The first half of the year is now in the rearview mirror. And, the first six months of 2024 marked one of the strongest rallies to start the year since the lead up to the dotcom bubble in the late 90s. The 14% surge in the S&P 500 during the first half has been largely dominated by just a few stocks – specifically those within the “AI Halo”. This dominance by just a few names has led to an increasingly narrow and historically concentrated market.

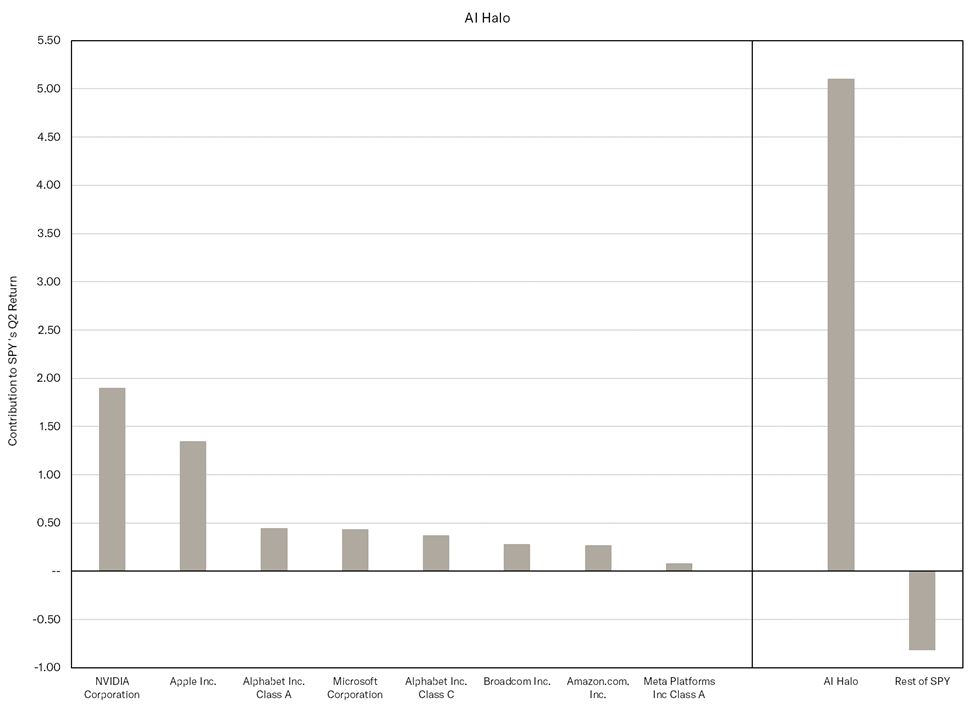

We wrote about this narrowness in last quarter’s Market Commentary as we discussed the outsized impact that the “Fantastic Four” (made up of Nvidia, Meta, Microsoft, and Amazon) were having on market performance. At the time, we also noted the surprising weakness in Apple’s performance through the first quarter. Sure enough, Apple turned things around in the second quarter. Now, nearly 60% of 2024’s gain has been driven by just five stocks: Nvidia, Microsoft, Amazon, Meta, and Apple. Nvidia itself has accounted for nearly 1/3 of the total gain year-to-date. In the second quarter that trend became even more pronounced as the AI-related stocks accounted for more than 100% of the market’s return. As a result, and as The Financial Times recently reported, the market would have been down in the second quarter were it not for the AI basket of names.

Source: FactSet

The SPDR S&P 500 ETF trust (SPY) is an ETF that attempts to track the S&P 500 stock market index.

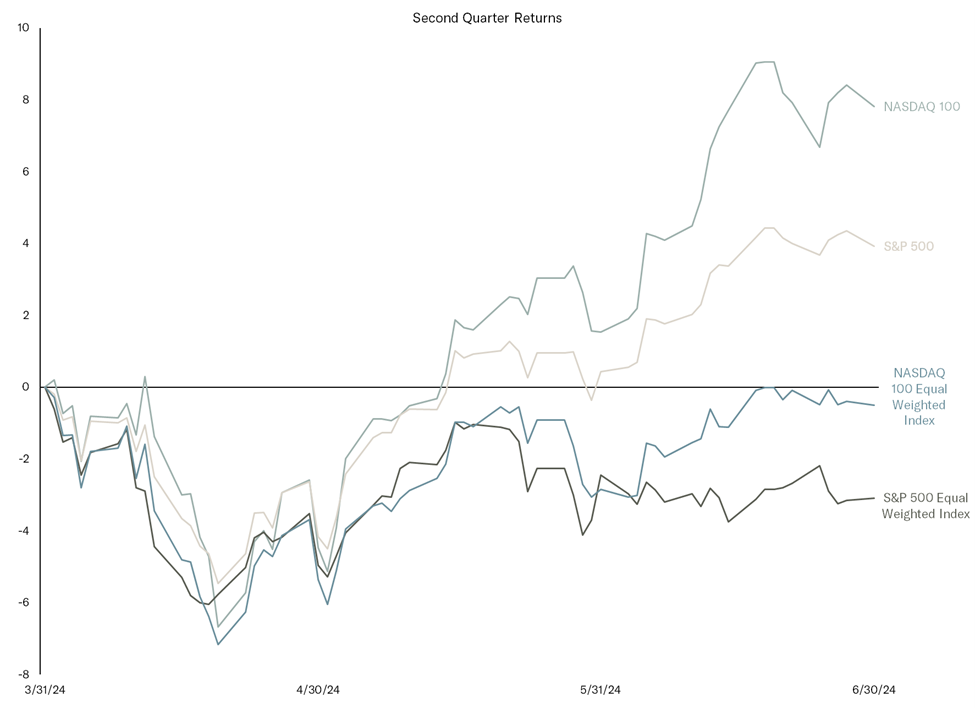

The narrowness of the market can be seen across the various indices as well. The tech-laden Nasdaq has returned nearly 70% since the end of 2022. The S&P 500 meanwhile has returned 42% over that same time frame. However, the S&P 500 Equal Weighted Index has gained just 16%. An equal weighted index can be viewed as a measure of the “average stock” within the index. The traditional S&P 500 weights stocks by their size, whereas the equal-weighted version treats all companies equally. For example, Microsoft accounted for more than 7% of the S&P 500 at quarter end. Within the equal weighted index, it’s more like 0.2% of the total index. The divergence between cap-weighted indices and their equal-weighted counterparts was even more apparent in the second quarter. For Q2, the Nasdaq 100 was up nearly 8%. The S&P 500 gained almost 4%. The Nasdaq 100 Equal Weighted Index and the S&P 500 Equal Weighted Index were both down. In other words, the big keep getting bigger while the average stock is lagging behind.

Source: FactSet

The dominance of AI is further amplified when one looks under the hood of the market as well. Unsurprisingly, Tech was the strongest sector in the quarter. Even more specifically, the semiconductor industry was especially strong and notched its place as the best performing industry for not just the quarter, but the first half. The nearly insatiable demand for chips in the AI race has created an environment that has allowed for semiconductor companies to absolutely soar.

Perhaps a bit more surprising was the strong performance of the utility sector in the second quarter. Utilities are often thought to be a defensive haven for investors. Utilities are now also believed to be a winner from the AI trade. AI computing requires the use of data centers to power the supercomputers and servers that allow AI to thrive. According to the Wall Street Journal, these warehouse-like data centers host servers that store cloud computing and process much of the data on the web. To do what it needs to do, AI computing demands massive amounts of energy to actually power and cool servers within these data centers. A recent report by Citi Bank claims that data centers could account for nearly 11% of all U.S. electricity demand by 2030 – more than doubling from its present 4.5%. The potential increase of demand in energy usage is considered to be a boon for some utilities who will reap the benefit of the electricity demand surges at these data center locations.

Finally, let’s talk about interest rates. By and large, interest rates remain elevated and mostly unchanged. 90-day Treasuries remain well above 5%, and the 30-day Treasury has yielded more than 5.3% for almost a year now. Quite remarkable given that the 10-year Treasury has been oscillating between 4% and 4.5% for much of the year. Unfortunately, or fortunately depending on one’s needs, it looks like there may be some downward pressure on rates in the future. The market presently believes that the Federal Reserve will lower interest rates in September, November, again in December, and possibly with an additional rate cut in the first quarter of next year. On the other hand, the market is often, often, often wrong with its interest rate predictions. However, should the interest rate scenario play out this way, one would expect to see interest rates begin to fall, especially when it comes to shorter maturities like a 30-day or 90-day Treasury, or perhaps even with rates offered on CDs. Unfortunately, the potential fall in short term rates does not necessarily mean that longer term rates will also fall. Shorter term rates are much more impacted by the Federal Reserve, whereas long-term rates are much more impacted by the free market, growth expectations, inflation expectations, etc. Long-term interest rates may fall. They may not.

Commentary— Historic Market? Or Challenging Market? Both Can Be True.

Good news! The stock market has been rallying to all-time highs. However, as we discuss in Market Commentary, the market’s recent performance has been the result of a historically concentrated market. The market’s recent superb performance is really due to just a few names. That’s not good news.

In our opinion, these recent trends have caused markets to become more challenging for managers like Tandem and a bit misleading to the everyday investor. First, as these few names have become increasingly more important to the performance of the S&P 500, it has led to a concentration within the index that is in no way the historical norm.

This has led to a distortion in the S&P 500, which has long been considered a gauge of how well the overall stock market is doing. Ordinarily, the S&P has broad diversification among its 500 components. Today, a small group of AI-related companies has become so large that it dominates the overall performance of the S&P, good or bad. The “average” stock in the S&P is not necessarily behaving like the S&P itself.

As the index becomes more concentrated it no longer provides the same gauge of the overall market because it instead becomes a gauge of just a few stocks! This leads to it becoming less diversified than it once was. For example, if someone were to buy SPY today, a commonly used ETF that is designed to track the S&P 500, they would effectively own an asset that has 31.56% exposure to AI through the likes of Microsoft, Apple, Nvidia, Meta and Alphabet. 10 years ago, the top names were Apple, Exxon, Microsoft, Johnson & Johnson, GE, Wells Fargo, etc. 10 years ago, the top holdings in SPY were diversified across industries and sectors of the economy. That seems less apparent today, which could be problematic for passive investors.

The second difficulty for most managers has been the absolute dominance by AI. The “AI Halo” has accounted for much of the market’s recent return. So, if one is not invested heavily in the “AI Halo”, then they have not been performing like the rest of the market.

According to Goldman Sachs, the 10 largest U.S. stocks now account for 33% of the index’s total market value – well above the 27% peak that was seen at the height of the Tech Bubble in 2000. By other metrics, this market is the most concentrated it has been since the early 1930s. To be frank, the causes of concentration in 2000 and 1932 were very different. 1932 marked a major bottom during the Great Depression, whereas 2000 marked a major market top. Today’s market probably has a bit more in common with 2000, or perhaps the concentrated market of The Nifty Fifty in the 70s. Like the late 90s and early 70s, unemployment is quite low today and the increased concentration within markets is occurring simultaneously with higher stock prices.

In the late 60s and early 70s, the Nifty Fifty consisted of blue-chip growth companies that were thought to be slam dunk “buy and hold” stocks. The Nifty Fifty stocks were growing faster than the market. As a result, they commanded a premium valuation relative to the rest of the market. Similarly, in the late 90s, technology was once more at the front of a social and economic revolution. This time, the internet was thought to be world changing technology. I think we can all agree that, by and large, the internet has changed the world – for the better most often, and occasionally for the worse. As a result of the dotcom boom, Tech stocks soared higher. Like the Nifty Fifty, anything web-related seemingly demanded premium valuations, simply because the companies were web-affiliated [see Pets.com or drugstore.com]. In the late 90s, the likes of Cisco, Microsoft, Dell and Intel were dubbed “The Four Horsemen” because of their undisputed market dominance. These four stocks remained dominant in their fields for years to come. However, their stock prices languished during the ensuing fallout after the bursting of the Tech Bubble.

Must this end poorly for today’s AI leaders, like it ended poorly for the Nifty Fifty in 1973 and dotcom stocks in 2000? Not necessarily. The AI stocks could just trade sideways for the foreseeable future. Or perhaps the rapid ascent could just slow down so that the rest of the market catches up. Either way, neither the dotcom bubble nor the Nifty Fifty were ideal times for many investors that were chasing the then popular trades of the day.

There is little doubt in my mind that AI will be revolutionary technology that will likely change the world in ways that we cannot presently fathom. I’m also fairly certain that we do not presently know who the winners and losers will be because all of the players have not necessarily emerged yet. The first smartphone was built by IBM in 1994 when the company released “Simon”. It featured email capabilities, among a handful of other apps. Blackberry then revolutionized the smartphone in 2002 taking it mainstream. Yet, I would imagine most readers of this newsletter likely have an iPhone in their pocket right now. Apple’s iPhone wasn’t released until 2007. It takes time for winners and losers to emerge and the first to the scene is not always the winner. I would be shocked if anyone is reading this newsletter from their IBM smartphone…

To date, Nvidia has been the leading beneficiary of the AI boom. The company’s chips lead the market when it comes to training generative AI models like ChatGPT. This boom led Nvidia to momentarily surpass both Apple and Microsoft as it briefly became the most valuable publicly traded company back in June. If you think of AI as being a gold rush, Nvidia is believed to sell the picks and shovels. Apple, Microsoft, Alphabet and Meta are all seeking different ways to implement AI and make AI consumer facing. But, Nvidia makes the hardware that allows for AI to become a reality. Hence, the market has begun placing a premium on Nvidia, as well as other suppliers within the AI rally.

However, it would seem that the AI rally could very well cannibalize itself. According to a recent Financial Times article, ~40% of Nvidia’s revenue comes from Microsoft, Meta, Amazon, and Google. How long will these companies continue to allow Nvidia to charge whatever Nvidia wants to charge? It seems unlikely that these tech behemoths will allow Nvidia’s sales, earnings and margins to rise in perpetuity. What seems more likely is that these companies will eventually build in-house server capabilities that make them less reliant upon Nvidia’s services. Just last year, Microsoft announced the launch of their own internal chips that, in time, will make them less dependent upon the likes of Nvidia. Meta, OpenAI, Amazon and Alphabet have all announced similar projects building their own AI processors. Likewise, Apple already announced that it would also be designing its own servers that would conceivably make their business less dependent upon companies like Nvidia. In other words, Nvidia could very well be having its Blackberry moment. They were the first big player into this market, but that doesn’t mean they will be the last.

It would not be surprising for the names within the “AI Halo” to continue to dominate the tech industry. However, the price being paid matters. Cisco, an oft-cited example of the exuberance of the late 90s, was dominant. Microsoft similarly dominated its competitors then, and continues to do so now. However, the prices paid for those stocks eventually mattered. Cisco has never surpassed its peak market value in the early 2000s. Meanwhile, it took Microsoft nearly 18 years to eventually surpass its Tech Bubble high. Nvidia has surged more than 2600% from its low during Covid in 2020. Is that sustainable?

At Tandem, we’ve always tried to say that we don’t look like the market. And we don’t necessarily always behave like the market, either. We don’t own Nvidia, nor do we own Alphabet, Apple, Amazon, or Meta. Sometimes not looking like the “market” is advantageous. Sometimes it’s not. We are not thematic investors. We do not chase the latest trends or ideas. We are not overweighting this stock or another because of some grand idea that someone here has. Ultimately, we try to own companies that can deliver a more consistent, more repeatable, and less volatile investment experience for our clients. To do that, we look for companies that can consistently grow earnings, sales, cash flow (and dividends) through any sort of economic environment.

Sometimes the companies that we seek to own fall out of favor when the market becomes fixated on some specific trade. Today it’s anything AI related. In ’21, it was unprofitable, disruptive, and hyper growth Tech (like the companies in the Ark funds). We won’t always perform in these sorts of one-dimensional markets because they are being driven by things that we don’t own. It doesn’t mean Tandem thinks AI stocks are bad stocks, or bad places to invest. Not at all. Most of these companies just do not meet our criteria today.

Tandem’s holdings by and large continue to do everything we ask of them – growing earnings, sales and cash flow. For whatever reason, the marketplace has its eye on something else. The market doesn’t appreciate our stocks nearly as much as we think it should! Given the discrepancy and absolute dominance by just a few stocks in the marketplace, there seem to be two obvious outcomes. First, the “AI Halo” could come back to earth to balance out recent performance. Or, everything else that has been left in the AI dust could catch up. Perhaps some combination of the two is most likely.

Regardless, we will continue to search for opportunities high and low to find stocks that are able to consistently grow the way we require. For more than 33 years, we have invested in this manner. Sometimes our stocks fall out of favor. Sometimes they are in vogue. Either way, we will continue to follow our discipline in our effort to deliver a more consistent, more repeatable, and less volatile investment experience because our clients have entrusted us with their own money to do exactly that. And we thank you for that trust.

Tandem News

Hello everyone! I have missed speaking with you all while I have been out on maternity leave. My husband, Ben (yes, the author of this piece!) and I welcomed our first child, John “Jack” Frederick Carew into the world in early June. We are thrilled – and maybe a little sleep deprived – but very happy and excited to have a new member of our family… and maybe one day another Tandem employee. “Start ‘em young”, as they say!

I look forward to reconnecting with you all again when I return to the office in September. Until then, our team is always available to support you, so please do not hesitate to reach out. I want to give a shoutout to our incredible Communications Team, of Ariel Davis and Paisley Lewis, as they have been the curators of Tandem’s recent LinkedIn posts, Commentary, and material releases. If you are not following us on LinkedIn already, I encourage you to do so to stay up to date on the latest Tandem news and more!

In other news, Tandem has grown once more! On June 3rd, Natalia Mattar joined the investment side of the business as our most recent associate. Natalia began interning for Tandem in May of 2023. She swiftly displayed a fantastic work ethic along with not just an eagerness to learn, but an ability to learn quickly. Natalia graduated from the College of Charleston in May 2024 with a Bachelor of Science in Finance and an Economics minor. When not in the office, Natalia enjoys staying active, running, and going to the beach with her Great Dane, Calie.

Until September – I wish you all a wonderful and safe summer season. Thank you for your partnership and trust in Tandem, as always!

– Elaine Natoli

Share:

Disclaimer: Tandem Investment Advisors, Inc. is an SEC registered investment advisor.

This audio/writing is for informational purposes only and shall not constitute or be considered financial, tax or investment advice, or an offer to sell, or a solicitation of an offer to buy any product, service, or security. Tandem Investment Advisors, Inc. does not represent that the securities, products, or services discussed in this writing are suitable for any particular investor. Indices are unmanaged and not available for direct investment. Please consult your financial advisor before making any investment decisions. Past performance is no guarantee of future results. All past portfolio purchases and sales are available upon request.

All performance figures, data points, charts and graphs contained in this report are derived from publicly available sources believed to be reliable. Tandem makes no representation as to the accuracy of these numbers, nor should they be construed as any representation of past or future performance.

Insightful Updates

Delivered

Timely and engaging information—right to your inbox.

More Commentary

Notes from the Trading Desk

U.S. stocks continued their march higher during last week’s holiday-shortened trading week. The S&P 500 finished the week at a record high and closed out the month of November 5.73% higher, its best monthly performance of the year, closing higher for the...

Notes from the Trading Desk

A post-election surge in U.S. stocks drove major equity indices to all-time highs last week. The S&P 500 surpassed 6,000 and logged its 50th record high of the year, while the Dow Jones Industrials Average crossed 44,000 for the first time.

Observations

Major U.S. equity markets experienced some consolidation in October after several months of upward momentum. The S&P 500 broke a streak of five consecutive monthly gains, declining 0.99%.